So what's wrong with living on credit?

It’s a HUGE gamble for us though, on the fact that we will continue to work to earn a living to pay off the credit. But what would happen if you could not work or your income stopped? You would struggle to pay your creditor and suddenly credit and loans are not so easily available..

When purchasing most large items such as a car or a house then you need some form of collateral or deposit.

How can I save when the cost of living is so high?

So how can I save if I have very little money left over each month? That is a key question most people ask, so we recommend you have a look at the videos below for some ideas, and you can also take a look at BudgetDrive.

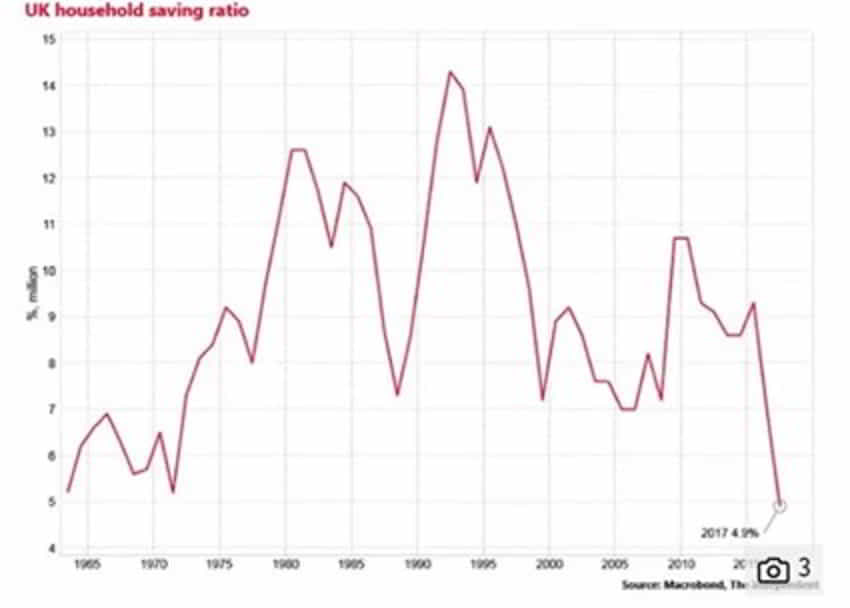

Why bother saving when UK Savings Rates are so low

Savings rates in UK have been extremely low over the last few years especially within banks. People are best doing regular medium saving plans and taking out best rate loans.

However, it's not only saving for future events - you can save to pay off your debts. These are both important goals, and you can work towards both at the same time. Also, there are times when you might need some money for emergency purposes (see below).

Different types of savings

There are 2 types of regular savings – long term 5-10 years plus and short-term savings with immediate access. It helps if you can save a small amount into an online account each month for those items 10 to 15 years ahead such as perhaps university fees or a special anniversary, weddings or special events.

Targeted savings for a purpose

Most people don’t have vast amounts of disposable income each month, therefore take a can’t be bothered attitude. When disposable income increases people well spend the money on more materialism. To make a real impact on saving a large amount of money requires a large monthly investment. Often people never get to this stage because they spend the cash on other feel-good factor items.

Rainy day savings

You do have to remember when taking out a savings plan what the risks are. Some schemes might offer higher rates of return but this may be riskier in terms of losing some of your money so it is important to read the fine print.

Kris Brewster, head of products for Skipton Building Society, which commissioned the research, said: “Having a healthy savings account is something everybody dreams of, whether it’s money put aside for a rainy day, helping fund your child through university or money saved for comfortable retirement.”