The dynamic housing market and how it has transformed lives

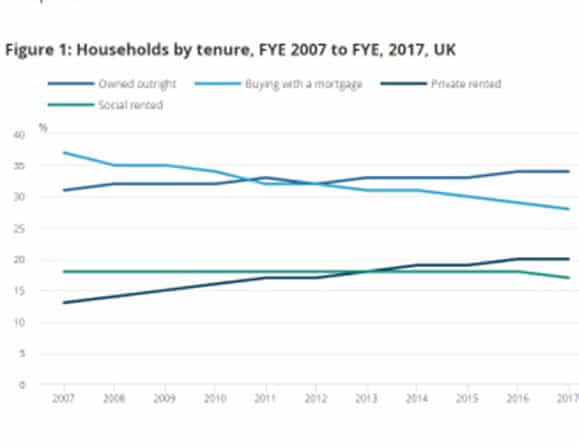

In the early 20th century less than 10% of UK homes were owner-occupied – this rose to 62% by the early 21st century, reaching over 27 million households in 2017.

Privately owned property is freehold or leasehold (where the owner buys the right to use the land and property for a time).

Most is bought with a mortgage. Since the 1980s securitisation of mortgages led to repackaging of mortgage debt to provide an income flow, which was involved in the 2008-9 financial crisis.

Property is also rented, either privately, where landlords typically use short term (often 6 months) tenancy agreements, or local authority rented, where tenants pay a weekly or monthly rent, often subsidised and below market rate. Housing Associations offer affordable properties partly owned partly rented.

The housing market

The housing market is an indicator of household wealth – when prices rise or fall it creates a positive or negative wealth effect, even as far as moving into negative equity, where the mortgage has a higher value than the house, as in 1990 and 2008. Rising equity can give rise to increasing housing equity withdrawal.

.

Other factors affecting home ownership include population, income, interest rates and social trends.

Social Housing

The amount of social housing for rent has been slowly rising for the last ten years – over 4 million homes were rented from councils or housing associations in 2017. Social rents are about 50% of market rents.

Housing associations are independent, not-for-profit organisations that provide social housing for people in need.. They are sometimes called ‘registered social landlords’. They sometimes offer shared ownership schemes and have to be registered with Homes England. They were re-classified as private rather than public in 2016, removing £70 billion form public debt and allowed them to increase borrowing.

This is mainly due to an increase in homes rented from housing associations. Around 5,000 new homes were built for social rent in 2017, and another 1,00 were bought or converted.

Governments policy on mixed community housing - does it work or is it a nightmare?

This heading sounds tame to be honest but it is the biggest social reengineering project that has taken place, ever. This is a government policy started back in the 90s when several projects were conducted around mixed community housing.

In simple terms instead of having defined areas where people of a certain group live and congregate such as council estates with generally lower income population and estates with elderly people living together. The Government ran several projects to aid the research on policy decision making. Over the last 25 years this policy has grown and developed into a life form and clearly has been modified and altered accordingly.

The feedback from many reports and reviews have been criticised because they are insufficiently evidenced based but have been emphasised positively to maintain government policy.

Different housing trends and how the market has changed over the years

Younger people are renting in preference to buying even though interest rates are low and mortgage offers are up to 95% and there are several government joint ownership schemes.

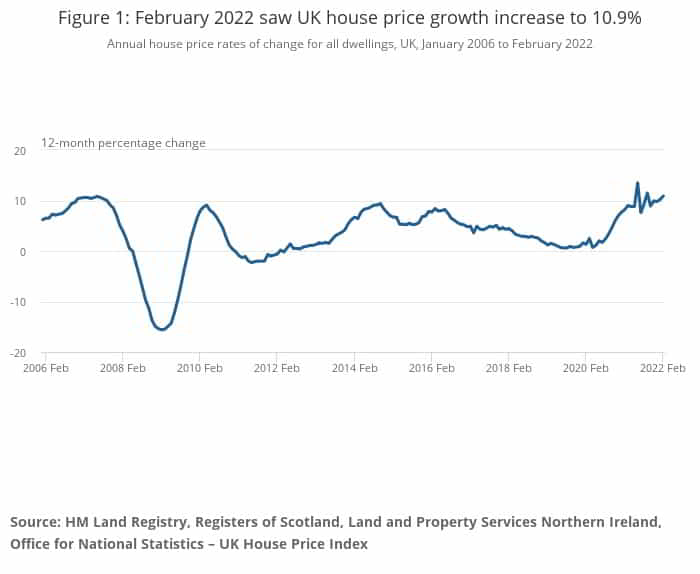

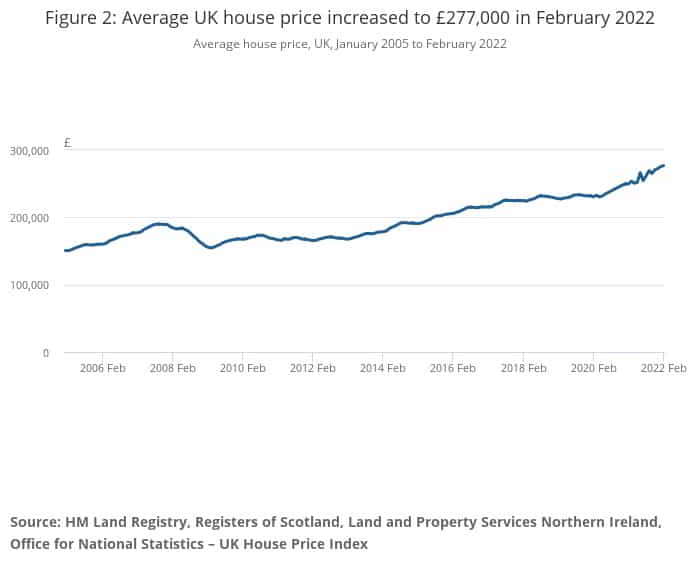

House Prices

You might be interested to know what's likely to happen to house prices. Money To The Masses explain what affects house prices:

The overall health of the economy: Unemployment and wage growth affect consumer confidence, which affects people's attitudes to moving and prices

Interest rates:The Bank of England set the base rate and if this is low people can afford to spend more which pushes prices up.

Supply and Demand: Local house prices are determined by a location's desirability and by how many similar properties there are.

The UK House Price Index is probably the most accurate measure as it is calculated on completed sales and includes cash sales and mortgages. There is however a time lag.Other indices include Nationwide, Halifax and Rightmove.

Buying a house is a win-win situation based upon the long-term market trends

When money is this cheap to borrow why wouldn’t you. Over a 30-year period if you earn good money and the latest mortgages only require 5% deposit then buying a home is a good investment. Especially when you consider that you house will increase without you doing a thing by on average 5 to 10% each year. .

If you buy a house in a good developing area that needs modernisation then you can make even more money after 5 years.

Why rent when you can buy - which is the best over the long term? Is it worth it?

The simple answer is that everyone’s circumstances are different. Some people have low paid employment and don’t meet the criteria for lending. Others have bad credit records or don’t have the deposit. Some people don’t like the scary responsibility of having a huge liability around their necks for 30 years. Whilst some people don’t want to be tied to a specific location and prefer to move around. Everyone is different.

Financially it seems to make sense to buy:

As a financial model buying is best because interest rates are low. The housing market in the UK is very progressive and always on the rise.

The average UK monthly mortgage repayment is £753.

Renting a property cost £821 on average.

If you can afford a mortgage, get one and buy a house. Try to buy a place that is resalable. Buy in a decent area. A property that may need a little bit of work doing to it and hang onto it for 5 years. In most instances you will make money.

However, it comes with strings attached:

See the video below.