Which mortgage is best for me

To answer that question, you need to obtain financial advice from a qualified Mortgage Advisor. But before you do that you need to understand more about the types of mortgages so that when you meet with an Advisor you are not clueless and need to take their words as gospel. The more informed you are the better the chances you have of getting the right mortgage.

The first thing to consider is your own position

Your family situation matters - are you buying a property with a partner, with children (existing or planned?

Is this your first mortgage, are you re-mortgaging your existing property or are you moving house?

Is the mortgage actually for a property you plan to live in, or is it for a property you intend to rent out (known as a buy-to-let mortgage)?

Then there's the type of mortgage - is the capital repaid at the end of the term or not (repayment or interest only), how is the interest rate set out (e.g. fixed or variable), and some specialist types of mortgage.

See some details in the tabs below.

Mortgages by purpose

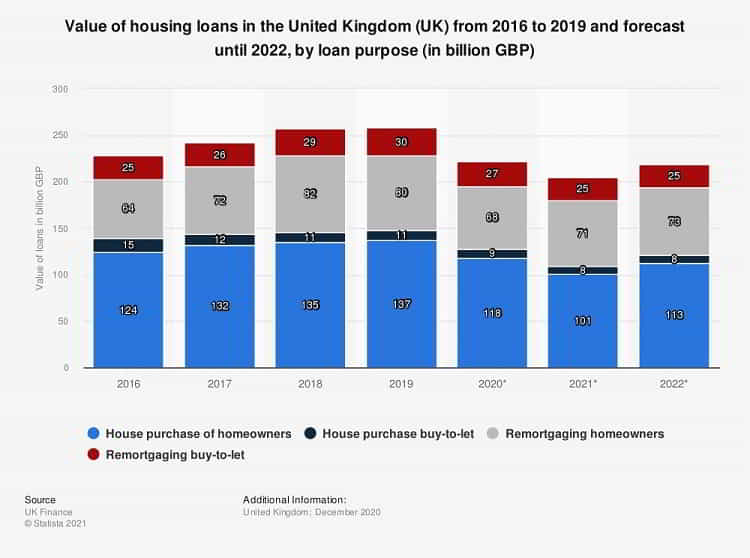

The chart here from Statista (sources FCA and Bank of England) shows the split between mortgages used for house purchase, remortgage, buy to let and buy to let remortgage.

Gross advances on residential loans issued to individuals in the United Kingdom (UK) from 2015 to the second quarter of 2021 in this statistic are distributed by loan purpose. In the second quarter of 2020, the share of house purchase loans dropped due to the coronavirus pandemic and the disruption of normal business activities. This share recovered in the following quarters and reached over 75 percent in the second quarter of 2021.

- Note the loans for house purchase dropped in Q2 2020 because of the pandemic, but recovered in the following quarters. So the %-age of mortgages for home ownership is again at pre-pandemic levels at 53.0%, down 10.9pp from 2020 Q4.(FCA)

- The share of gross advances for remortgages for owner occupation also moved towards levels observed before the pandemic, at 28.1%, an increase of 9.7pp since 2020 Q4.(FCA)

- The outstanding value of all residential mortgage loans was £1,613.4 billion at the end of 2021 Q4, 4.7% higher than a year earlier.

- The value of gross mortgage advances in 2021 Q4 was £70.2 billion, 8.4% lower than in 2020 Q4 as shown above in Facts, and this is the lowest level since 2020 Q3.

Click on any of the tabs on the right to see more information

What is a variable rate mortgage?

A variable rate mortgage is a type of mortgage in which your interest rate, and in turn your monthly repayments, can go up or down.

Variable rate deals fall into 3 main categories – standard variable rates (SVRs), tracker rates and discounted rates.

SVR – each lender has its own SVR which it can change at any time, so your payments could go up!

Discount mortgages use the SVR with a fixed amount discounted. So if the SVR was 4% and your discount was 1.5% you’d pay 2.5%. The discount can be stepped, or limited by rate or time period – check this!

Tracker mortgages – your interest rate ‘tracks’ the Bank of England base rate – you might pay the base rate plus 3% (3.75%). You’d typically have a tracker for a set period then revert to SVR or another special deal, but there some lifetime trackers.

Discount mortgages use the SVR with a fixed amount discounted. So if the SVR was 4% and your discount was 1.5% you’d pay 2.5%. The discount can be stepped, or limited by rate or time period – check this!

Discount mortgages use the SVR with a fixed amount discounted. So if the SVR was 4% and your discount was 1.5% you’d pay 2.5%. The discount can be stepped, or limited by rate or time period – check this!

Also the rate you pay will be determined by your lender and can move up and down, so you may not know the exact figure coming out of your account every month.

Here you typically pay the fixed rate for the entire period of the mortgage deal – say 3 or 5 years, then revert to the SVR.

Clearly if interest rates go up these are beneficial, especially if you’re on a budget.

Here you pay some of the capital (loan amount) with an interest payment each month. As you repay capital each month the next interest payment is lower, so you repay more of the capital as time goes on.

If you keep up the payments you will be guaranteed to repay the mortgage by the end of the term.

These are the most common type of mortgage, especially for home ownership.

With an interest-only mortgage you only pay interest each month. You don’t pay off any of the capital until the end of the mortgage term, when you have to pay the entire loan amount back.

Interest-only mortgages are usually only available on buy-to-let properties. If you want to take out an interest-only mortgage, you’ll need to make other arrangements for paying back the capital. This is known as setting up a separate ‘repayment vehicle’, which can be investment, such as a stocks and shares ISA or pension.

You need to ensure that the money you’ve invested elsewhere will be enough to fully pay off the mortgage when the term ends. You may be able to guarantee this amount from existing savings.

Your monthly payments will be less each month as you don’t repay capital. You’ll pay more in total for an interest-only mortgage as you’re paying interest on the entire loan each month (with a repayment mortgage the amount of interest you pay reduces as you repay capital).

Flexible mortgages let you over and underpay, take payment holidays and make lump-sum withdrawals. This means you could pay your mortgage off early and save on interest.

You don’t normally have to have a special mortgage to overpay, though; many ‘normal’ deals will also allow you to pay off extra, up to a certain amount – typically up to 10% each year. mortgages, where your savings are used to offset the amount of your mortgage you pay interest on each month.

Flexible deals can be more expensive than conventional ones, so make sure you will actually use their features before taking one out.

A buy-to-let mortgage is a type of home loan for buying property that you intend to rent out to residential tenants for a profit. Most buy-to-let mortgages in the UK are interest-only, with the landlord paying the monthly interest using rental income.

Buy-to-let properties come in all shapes and sizes, from houses to apartments and everything in between. Unless you own a property outright, it is usually against your lender’s rules to rent it out without taking out a BTL mortgage.

An arrangement whereby a person takes out a mortgage and pays the capital repayment instalments into a pension fund and the interest to the mortgagee. The loan is repaid out of the tax-free lump sum proceeds of the pension plan on the borrower’s retirement.

Government backed mortgage scheme

Lifetime Individual Savings Account (LISA)

You can use a LISA to buy your first home (for a property costing £450,000or less) or save for later life. You must be aged between 18 and 39 to open a LISA.

You can put in up to £4,000 each year, until you’re 50. You must make your first payment into your ISA before you’re 40. The government will add a 25% bonus to your savings, up to a maximum of £1,000 a year.

If you’re buying with another first-time buyer who also has a LISA, you can both use your LISA towards the same property.

Be aware that there’s a penalty for taking money out of a LISA if you’re not putting it towards a deposit or withdrawing after age 60.